Cashless is the new green: Future of digital payments

Meha Savla

01 Dec 2025

There was a time when forgetting the wallet at home meant signing up for an entire day’s ruckus. You can either borrow money from a friend or manage to get your wallet. Else you’re on your own, kid.

Then there was an age where cards were the new currency. A new era for India to embrace and celebrate.

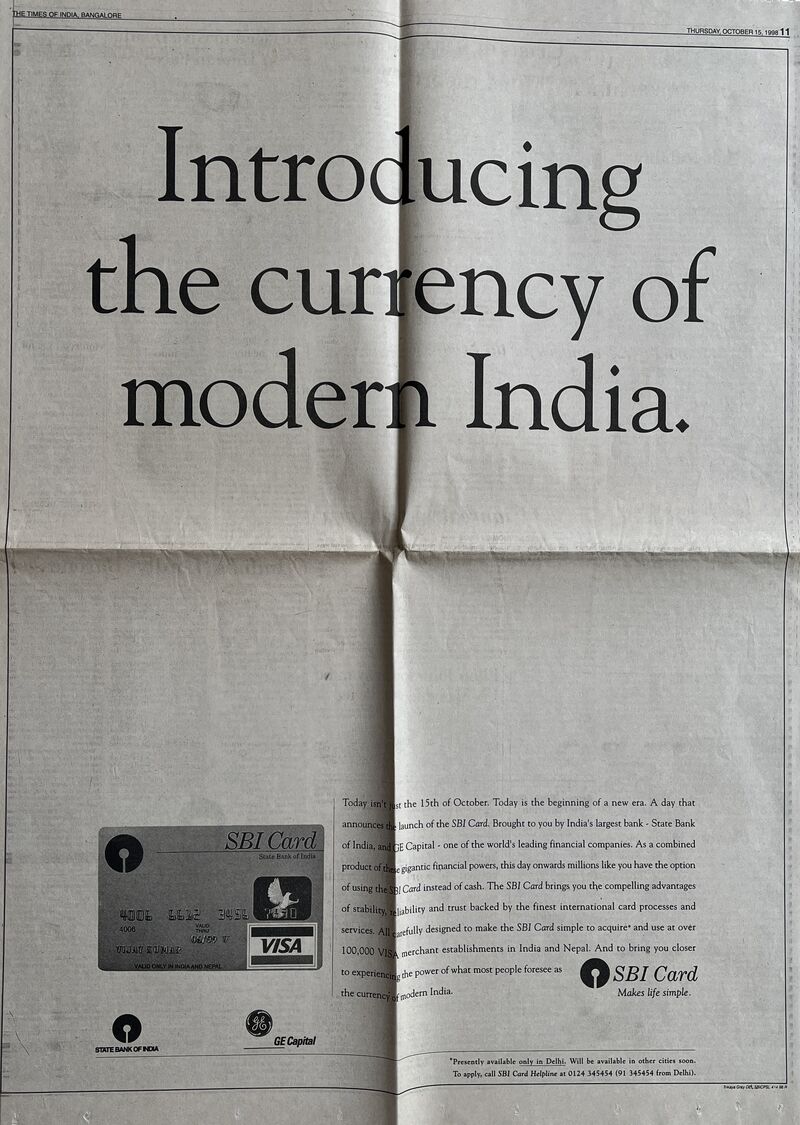

The brainchild of Prathap Suthan (and team) to market SBI Card, October 1998.

Cut to today, when bags come in sizes two times smaller than a traditional wallet, indicating that they’re no more an “essential”. And that is only possible with a digital revolution, one that has now taken the front stage.

More than digital, it is the era of a cashless revolution. A recent report by Kearney and Amazon Pay India states that 90% consumers with internet access choose digital payments for online purchases.

What does this mean for the fintech industry?

Well, a great success, obviously. But there’s more to it:

Trust on fintech

Users are not skeptical about making online payments. They trust the mode of digital payment, as well as the brands they’re making the payment to. Overcoming this initial stage of hesitation and building trust in fintech is a great deal, especially in a money-conscious country like India.

Convenience over all else

Among the many requirements and parameters of user satisfaction, convenience tops the list. Speed and rewards also play a role, of course, in resorting to digital payment methods. But the sheer ease of completing transactions online is a reward in itself.

Age is just a number

The study showed Millennials (aged 25 to 43) and Gen X (aged 44 to 59) are majorly adopting many and all types of digital payment methods. Fluency in using these apps doesn’t seem much of a task either, across different generations.

Gender equality

Like age, gender doesn’t stand out as a differentiating factor either. The digital payments ratio of men to women is almost 1:1.

Small and big towns alike

Yet another (almost) equalizing factor is cities. Mid-sized cities reach the digital payment mark with 65% transactions, close to the 75% in metro population. The rapid pace of digitization, thus, goes beyond metro areas, with cities like Lucknow, Bhopal, Jaipur, Pune, Ahmedabad far ahead in the race.

Street to store

Local grocery vendors, autorickshaw drivers, and kirana stores have embraced digital payments wonderfully. Half of them, if not most, receive the majority of their payments online. This makes business easy, not only at the payment stage, but also to maintain a proper record of the transaction history too.

What does all of this really mean for fintech?

The report shares highlights as well as opportunities that lie ahead of financial institutions to continue building on the growing landscape of fintech.

Calls for more security

Security remains of utmost importance to the financial domain. And the industry in modern times is having modern problems. With the rise of online banking, cases of financial fraud have gained increased attention too. Advanced false documentation screening, among other cybersecurity algorithms that detect fraud, are the need of the hour.

Taking screenshots was always easy on WhatsApp, all until the platform denied capturing screenshots of display pictures. Like OTT platforms, WhatsApp considers display pictures as the owner’s private data, as it should. So now, on taking a screenshot, the system only loads a blank black screen. Data encryption done right. Protecting users’ data is taking priority in every industry, and most importantly, in fintech.

Role of FinteD

More than anything else, all fintech products have two things in common: the industry, as well as its regulations and compliances which usually dictate how the platforms are required to be. However, platforms follow different onboarding and know-your-customer (KYC) processes.

By adding design to fintech, brands can create onboarding journeys that are more streamlined across different platforms. By optimizing with a clean, easily navigational user interface, brands can collectively (yet individually) build smoother user journeys. Something FinteD aims to achieve.

Scope of financial literacy

Access to fintech products and knowledge of their benefits majorly affects how users interact with them. Payments are but only one sector in the entirety of fintech. There are growing numbers of digital products, including portfolio and wealth management, among others.

Most of these products remain underutilized by the larger population, solely due to lack of proper knowledge and resources. There is, thus, vast scope to educate people about investing, budget management, insurance, etc., with interactive video lessons, data visualization techniques and more.

Ecosystem of fintech

Super apps have already entered the fintech industry, and how! Additionally, newer methods and systems of payment are bracing the industry, crafted with innovation and convenience in focus - as is usually the case with fintech products.

Compatibility with emerging technologies like wearables, voice-assistant technology, and even the Buy Now Pay Later (BNPL) offering, will lead to building a holistic ecosystem of banking and financial services. Institutions have the potential to go above and beyond, to offer the choicest of solutions that keep up with the age, time and needs of the users.

The report is a testament to the progress the industry has made in the many years: an account of how far it has come and the long path ahead, full of opportunities.

The future of digital payments? Digital payments are the future - bright and digital.

Sharing is caring